Getting funds at the right time is critical for many growing businesses. Whether you’re just starting out, breaking into new markets, developing products or expanding your workforce, a business loan or grant can provide the capital you need.

One good option is to choose a loan backed by the Small Business Administration (SBA). The SBA is a U.S. government agency dedicated to supporting small businesses, and one of the main ways they do this is by guaranteeing loans from SBA lenders.

But how do you choose the right SBA-approved lender for your business? We’re here to help. We’ve researched several of the best small business lenders so you can find the perfect one for your business needs. We’ll start by exploring some common requirements for taking out an SBA loan, then dig into specific offerings from lenders approved by the SBA.

How SBA-Approved Lenders Decide to Let Your Business Borrow Money

Demand for SBA loans is high, and approved lenders have strict criteria for lending out money. Although specific requirements do vary slightly between SBA lenders, here are some of the common areas they look for.

High Business or Personal Credit Score

Your credit score shows how reliable you will be at repaying a loan based on your previous borrowing and repayment history. SBA lenders are looking for businesses with high credit scores that demonstrate a low risk of defaulting on loan payments.

If you have a Dun & Bradstreet number and profile, then a lender may use that to determine your business credit score. Otherwise, they are likely to use the owner’s or founder’s personal credit score.

Strong Cash Flow and Financial Statements

Your business must have enough free cash flow to comfortably make its loan repayments. SBA lenders will look carefully at your cash flow statements, profit and loss, balance sheets and other financial reports.

Showing strong financial management, together with low amounts of existing debt, will improve your chances of loan acceptance.

Personal or Business Assets for Collateral

One way that SBA lenders reduce the risk of defaults is to require “collateral” from you or your business. That way, if your business fails to make repayments and defaults on the loan, the lender will seize and sell the assets to recoup their losses.

Collateral can take many forms — bank accounts, property, inventory or other assets, and the better the collateral you can provide, the greater your chances of getting accepted.

Mature Business with a Proven Track Record

SBA-approved lenders prefer to lend to businesses that have a good track record — whether that’s time in business, previously paying back loans or a history of good financial choices and growth. Typically, lenders will want to see that you’ve been in business for at least two years, and the longer, the better.

How Do I Choose an SBA Lender?

The SBA provides a list of its top 100 lenders, in descending order of the total value in loans that they have approved. We looked at the top 10 best small business lenders on that list, and we’ve shared our findings below. Take a look, and decide on which one is best for your needs.

What Is the Easiest SBA Loan to Get?

Requirements do vary between lenders. We’ve listed out some of the most common criteria above, and we’ve gone into more detail in our review of each of the lenders below. We recommend reviewing their websites in detail and speaking to their loan specialists to find out if your business qualifies for an SBA loan.

The Top 10 SBA-Approved Lenders

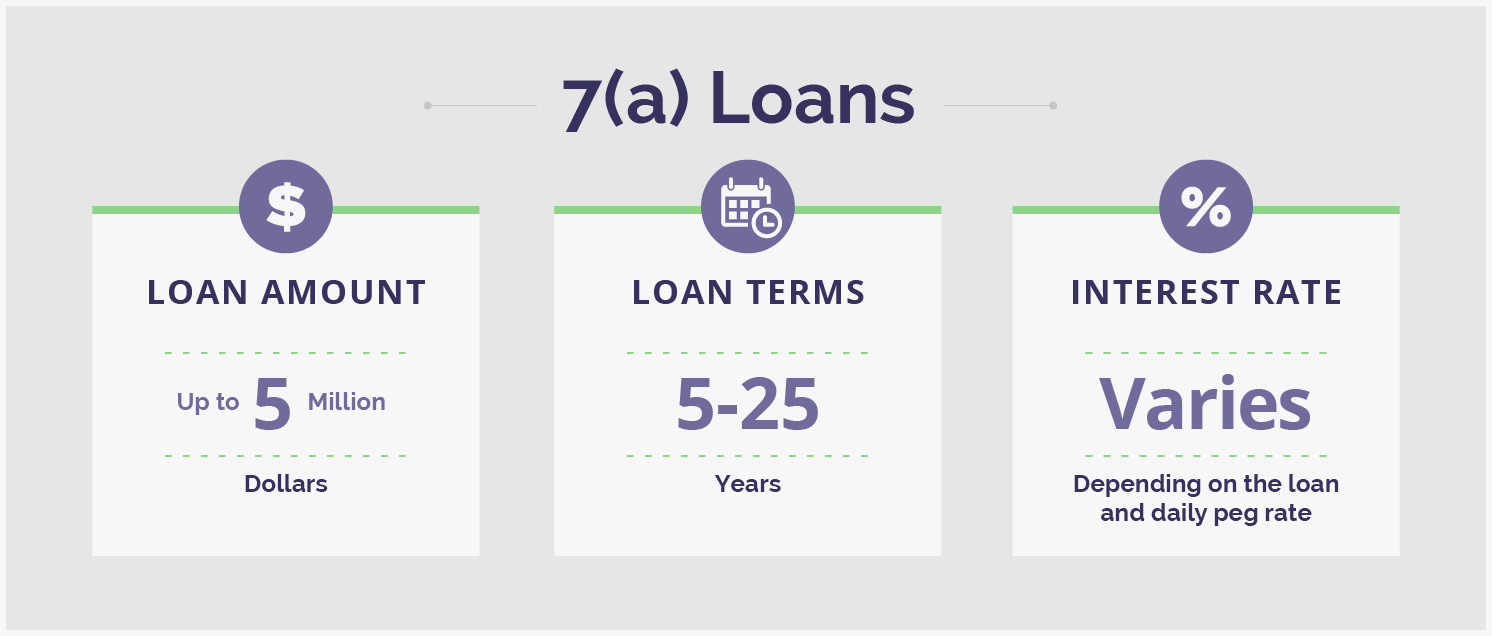

Here’s our breakdown of the top 10 lenders by SBA loan approved amount value. Many SBA lenders do provide different types of approved loans. In our breakdown, we’ve mainly focused on the most popular SBA 7(a) loans, but other loan types may be available.

We’ll also note that the 25-year repayment terms mentioned are mainly available only on real estate loans. SBA loans for other purposes often have to be rapid much sooner. Visit their websites for more information.

These top 10 SBA-approved lenders are a great starting point for seeking out business financing.

For more help with your business's finances, Incfile can assist you with your bookkeeping and accounting.

Paul Maplesden

Paul is a freelance writer, small business owner, and British expat exploring the U.S. When he’s not politely apologizing, he enjoys hats, hockey, Earl Grey Tea, mountains, and dogs.