If you've ever had an employer-provided retirement account, then you know firsthand how convenient they can be. With such a plan, you make contributions, your employer makes contributions and your retirement fund quietly grows in the background.

But with self-employed retirement plans, things get a lot more hands-on. If you want one, then you'll have to choose which kind of plan to open and exactly how much to contribute.

So what type of retirement plan is primarily for self-employed people, and which plan should you choose? To get your financial planning in order, we'll explore all the best self-employed retirement plans ahead.

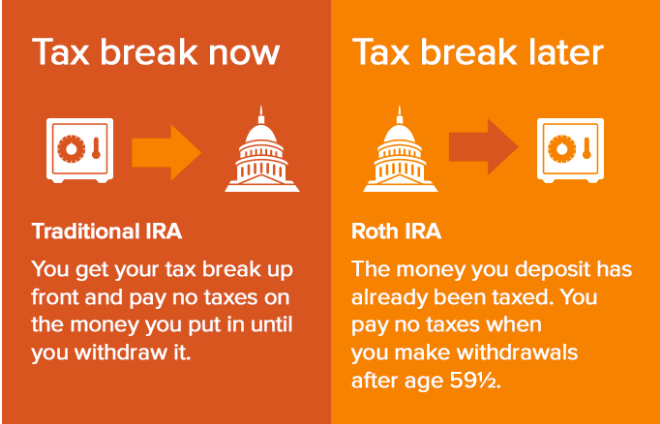

Roth or Traditional IRA

Individual retirement accounts, or IRAs, are a natural starting point for your research into self-employed retirement plans. You can run an IRA completely independently of an employer, whether you're self-employed or not, so contributing to it is simple.

The main differences between Roth and traditional IRAs include the following:

- Contributions to traditional IRAs are tax-deductible the year they're made, while contributions to Roth IRAs are not tax-deductible.

- Withdrawals from traditional IRAs are taxable even in retirement, while qualified withdrawals from Roth IRAs are tax-free in retirement.

If you can't decide whether you want your tax benefits now (with a traditional IRA) or later (with a Roth IRA), check the IRS' eligibility requirements first — they might just make the decision for you.

One-Participant 401(k)

Also referred to as a solo 401(k), individual 401(k) or uni-k plan, a one-participant 401(k) is identical to a traditional 401(k) plan in many ways. The two main differences are that you'll serve as both employer and employee, and you won't be subject to discrimination testing.

As the IRS explains, when you have a one-participant 401(k), you can contribute both:

- Elective deferrals up to 100 percent of earned income up to the annual contribution limit of $19,500 (2020-2021)

- Employer nonelective contributions up to the maximum contribution limit of $58,000 (2021), plus up to $6,500 in additional contributions for those aged 50 or older

So, you can effectively contribute much more than you'd be able to with a 401(k) sponsored by an employer. As an added bonus, you can choose either a standard 401(k) or Roth 401(k), which means you can choose whether you want to make contributions pre- or post-taxes.

Want to figure out how much you'd be able to contribute to your own one-participant 401(k)? Use the worksheets found in chapter five of the IRS' Publication 560, Retirement Plans for Small Businesses.

Simplified Employee Pension (SEP)

As its name suggests, a SEP IRA gives people a simple, straightforward way to reap the benefits of a self-employed retirement plan without the fees and operational challenges that can be associated with other, more complicated options.

If you're self-employed, you can contribute up to 25 percent of your net earnings from self-employment, up to $58,000 in 2021.

SEP IRAs have several unique benefits:

- You only need to fill out a brief one-page form called 5305-SEP to establish a SEP IRA

- Easy for individuals to operate and administer without any associated fees

- Allow for flexible contributions

Plus, if you avoid using Form 5305-SEP and instead adopt a prototype or individually designed SEP, you'll also be able to have another type of retirement plan such as a 401(k).

SIMPLE IRA

A Savings Incentives Match Plan for Employees (SIMPLE IRA) is unique in that it allows you to contribute all your net earnings, up to a certain amount depending on the year.

You can also put in an additional $3,000 per year (2015-2021) if you're 50 or older, as well as either a 2 percent fixed or 3 percent matching contribution.

SIMPLE IRAs can be beneficial because they:

- Are easy to set up via forms 5304-SIMPLE and 5305-SIMPLE

- Don't require the same fees and administration as traditional 401(k) plans

- Aren't subject to discrimination testing

However, SIMPLE IRAs have rigid contribution amounts and aren't allowed to be used in tandem with other types of self-employment retirement plans, both of which are limitations to consider before making a commitment.

Defined Benefit Plans

If you're self-employed, then a defined benefit plan is essentially a pension plan that you set up for yourself. By doing so, you'll give yourself a guaranteed income stream come retirement time.

The exact amount of money you'll receive after you retire typically depends on two things:

- Your salary

- The number of years you spent working at your business

As far as advantages, defined benefit plans can be used alongside other self-employed retirement plans, can generate a substantial amount of money within a short time frame and offer guaranteed benefits.

But defined benefit plans aren't without their downsides — they're the most costly type of retirement for self-employed people, require the most administrative effort and can be subject to excise taxes.

How Does a Self-Employed Person Save for Retirement?

If you're wondering how to save for retirement when you're self-employed, then you're asking the right questions. It's one thing to know which types of self-employed retirement plans are available, but it's another thing entirely to choose one and start setting aside money.

So when you're evaluating which plan to go with and how to start making contributions, you should consider your age, income, business, wants and needs.

- If you're on the younger side or have recently started your business, you'll likely benefit most from a Roth or traditional IRA.

- If your business consists only of you and possibly your spouse, and you expect to have a substantial amount of money to save, a one-participant 401(k) might be the best fit for you.

- If you have no or few employees and want a straightforward retirement plan, a SEP IRA could be right up your alley.

- If your business has 100 or fewer employees and you want a low-cost way to support both your and their retirements, a SIMPLE IRA may be an ideal choice.

- If you earn a very high income, have no employees, can afford high startup and administrative fees and are close to retirement, you might want to consider a defined benefits plan.

While choosing and setting up your own retirement plan might not be your idea of fun, you'll certainly be glad you did.

For every other aspect of your business, there's Incfile. We've helped more than 1,000,000 businesses get their start and continue to grow, and we can help yours too.

Carrie Buchholz-Powers

Carrie Buchholz-Powers is a Colorado-based writer who’s been creating content since 2013. From digital marketing to ecommerce to land conservation, she has experience in a wide range of fields and loves learning about them all. Carrie is fond of history, animals and beauty in equal measure. In her free time, she enjoys knitting, playing video games and exploring Colorado's prairies and mountains with her husband.